What Are Supply and Demand?

Taught in US schools

Key Takeaways

- Supply is how much of a good or service is available; demand is how much consumers want to buy.

- When demand is high and supply is low, prices tend to rise; when supply is high and demand is low, prices tend to fall.

- Market equilibrium is the point where the supply of a product matches the demand for it - the 'sweet spot' for a price.

What Are Supply and Demand?

Supply and demand are the two forces that drive how markets work and how prices are determined. They are the foundation of economics - the study of how people and societies make choices about using resources.

-

Supply = how much of a product or service is available for people to buy

-

Demand = how much consumers want to buy of that product or service

What Is Supply?

Supply refers to the amount of a product or service that producers are willing and able to make available at a given price.

Supply can be:

-

High - lots of the product available (e.g., tomatoes in summer when crops are plentiful)

-

Low - limited amounts available (e.g., a rare video game sold in limited quantities)

What affects supply?

- Cost of materials and labor

- Technology and production efficiency

- Natural events (drought, storms reducing crops)

- Number of producers in the market

What Is Demand?

Demand refers to the desire and ability of consumers to buy a product or service at a given price.

Demand can be:

-

High - many people want it (e.g., a popular new toy before the holidays)

-

Low - few people want it (e.g., the same toy a year later)

What affects demand?

- Consumer preferences and trends

- Price of the product

- Income of buyers

- Availability of alternatives

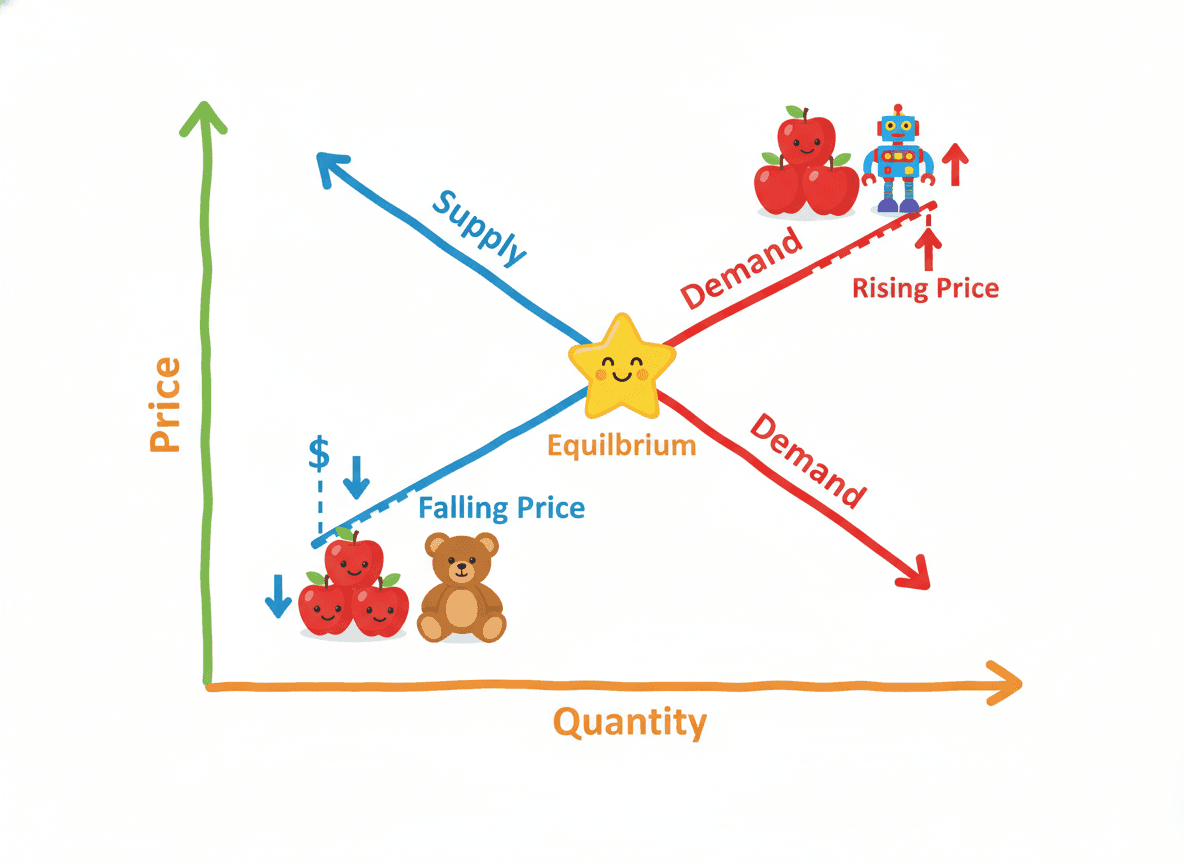

How Supply and Demand Affect Price

The relationship between supply and demand determines the price of goods and services:

High demand + Low supply: Price rises

Low demand + High supply: Price falls

Demand = Supply: Price stays stable (equilibrium)

Lemonade stand example: If it's a hot day and many people walk by (high demand), you can charge more for your lemonade. If only a few people walk by (low demand), you might lower your price to attract buyers. If another lemonade stand opens next to yours (more supply), you might have to lower your price to compete.

Market Equilibrium

Market equilibrium is the point where the quantity producers want to sell matches the quantity consumers want to buy at a given price. At equilibrium:

- No surplus: producers are not left with unsold goods

- No shortage: consumers can find what they want at that price

Markets are constantly shifting toward equilibrium as prices adjust.

Scarcity and Economics

Scarcity - having limited resources to meet unlimited wants - is the basic economic problem. Supply and demand are tools for allocating scarce resources:

- When something is scarce and wanted, its price reflects that scarcity (high price).

- When something is abundant, prices are lower.

Real-World Examples for Students

Popular toy before the holidays: Low - Very High - Price rises

Strawberries in summer: High - Moderate - Price falls

Gasoline during a shortage: Low - High - Price spikes

Old phone model after new one released: High - Low - Price drops

Practice Activities

- Run a "classroom economy" simulation: create products (bookmarks, drawings), set prices, and observe how prices change based on how many students want them.

- Role-play a lemonade stand scenario where weather changes the demand; students adjust prices accordingly.

- Graph a simple supply and demand scenario using data provided on a worksheet - identify the equilibrium point.

- Research: why do plane tickets cost more during the holidays? Connect to supply and demand.

- Debate: should there be laws limiting how much companies can charge for essential goods during emergencies (price gouging)? Use supply-and-demand reasoning.

Frequently Asked Questions

What is a real-world example of supply and demand for kids?

Think about a popular toy at holiday time. Before the holiday season, demand is very high - everyone wants it. If the factory cannot make enough (low supply), stores run out and the price may go up. After the holidays, demand drops - fewer people want it - and stores may put it on sale to clear their shelves. The price dropped because demand fell while supply stayed the same.

What is market equilibrium?

Market equilibrium is the point at which the quantity of a good that producers want to sell matches the quantity that consumers want to buy at a given price. At equilibrium, the market 'clears' - there is no surplus (too much unsold product) and no shortage (not enough product to meet demand). Equilibrium prices shift when supply or demand changes.

How does scarcity connect to supply and demand?

Scarcity means there is not enough of something to satisfy everyone who wants it. Scarcity is what creates demand. When a resource or product is scarce (low supply) and many people want it (high demand), prices rise. Unlimited supply of something with no demand creates no economic value. Economics is largely the study of how people make choices in a world of scarcity.

Free Supply and Demand Worksheets

Curriculum-aligned printable worksheets for 4th – 5th Grade. Download free.